基于层次分析法的EVA财务绩效优化

——以D公司为例

打开文本图片集

【摘 要】不管是经济增加值(EVA)还是考虑资本投入后的EVA报酬率都只能作为单一财务评价指标,无法深入探究企业价值增值背后的驱动因素。论文对EVA指标公式逐层分解,归纳影响价值增值的驱动能力,引入企业绩效评价标准,结合案例公司财务数据运用层次分析法开展财务评价。

【Abstract】Both economic value added (EVA) and EVA return rate after considering capital input can only be used as a single financial evaluation index, and cannot deeply explore the driving factors behind the enterprise value appreciation. In this paper, the EVA index formula is decomposed layer by layer, which summarizes the driving ability to affect the value appreciation, introduces the enterprise performance evaluation standard, and uses the analytic hierarchy process combined with the financial data of case company to carry out the financial evaluation.

【关键词】层次分析法;经济增加值(EVA);驱动因素;财务评价

【Keywords】analytic hierarchy process; economic value added (EVA); driving factors; financial evaluation

【中图分类号】F275 【文献标志码】A 【文章编号】1673-1069(2022)02-0137-04

1 引言

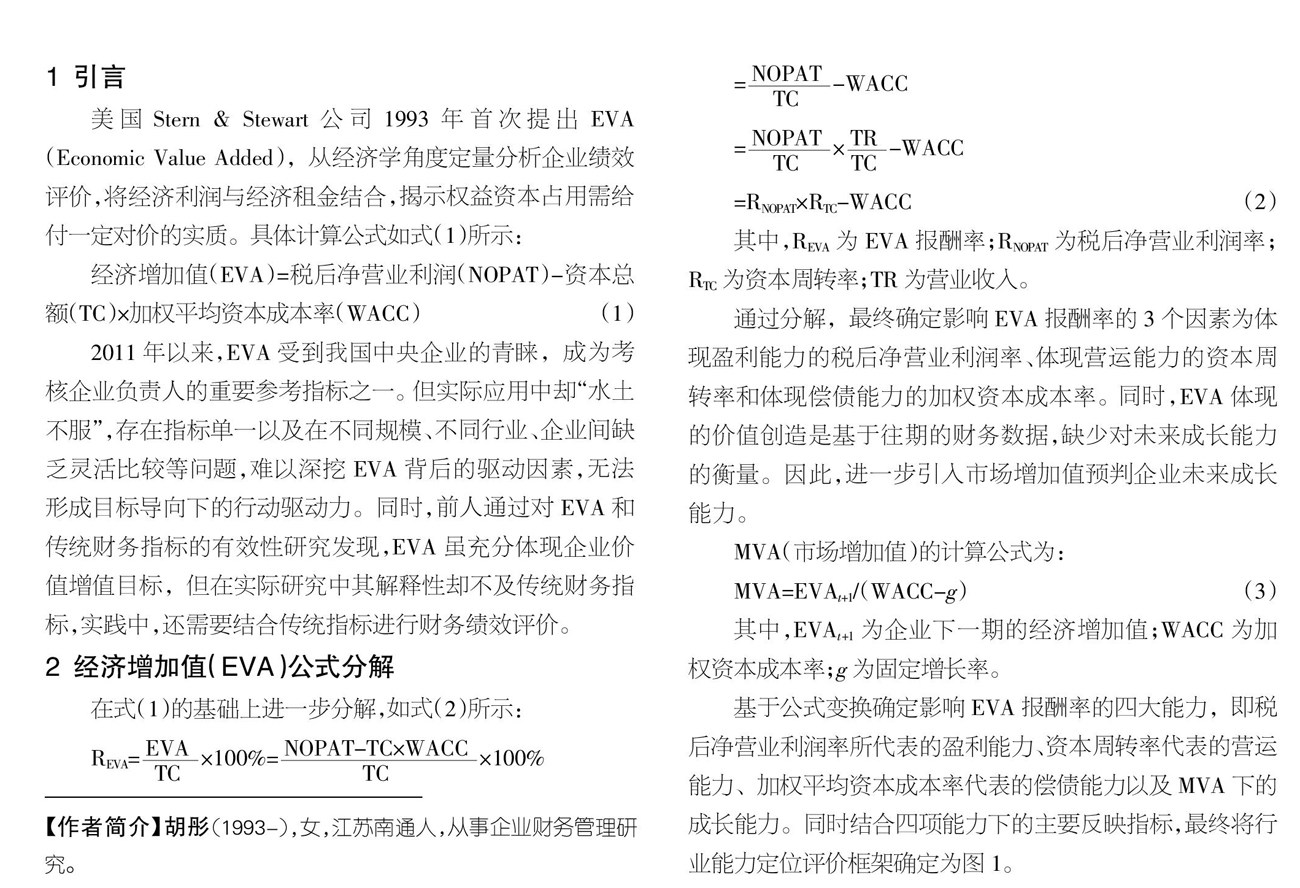

美国Stern & Stewart公司1993年首次提出EVA(Economic Value Added),从经济学角度定量分析企业绩效评价,将经济利润与经济租金结合,揭示权益资本占用需给付一定对价的实质。(剩余4137字)